In the recent past, there has been a lot of discussion in the builder community on Affordable Housing vis a vis the Income Tax deduction as per the provisions of Sec 80-IBA of Income Tax Act.

Let me take this opportunity to decode the above statement by bringing to your notice that the above statement is a combination of two different provisions.

Firstly, the provision of Sec 80-IBA of Income Tax Act which speaks about the deductions in respect of profits and gains from housing projects.

Secondly, a notification no. 13/6/2009-INF issued by the Ministry of Finance dated 30th March, 2017 which incorporates a new sub sector "Affordable housing" under the category of "Social and Commercial Infrastructure"

Now, lets understand the conditions imposed under sec 80-IBA to claim a deductions in respect of profits and gains from housing projects

Majorly, the conditions of 80-IBA can be divided into six categories, detailed as below

A. PROJECT

Notification no. 13/6/2009-INF issued by Ministry of Finance dated 30th March, 2017

Thus, a net inference from the conjoint reading of both the clauses i.e., to develop an affordable housing and claim the benefit of profit deduction u/s 80-IBA, will be something like this -

MASTER STROKE by the central government of India in defining affordable housing with FAR utilisation of 50% with a restriction of 60 sqm carpet area AND giving benefit u/s 80-IBA with a FAR utilisation of 90% / 80% and a restriction of 30 / 60 sqm of carpet area within the cities of Mumbai (B), Kolkata (C), Delhi (D), Chennai (C) and any other places respectively.

Let me take this opportunity to decode the above statement by bringing to your notice that the above statement is a combination of two different provisions.

Firstly, the provision of Sec 80-IBA of Income Tax Act which speaks about the deductions in respect of profits and gains from housing projects.

Secondly, a notification no. 13/6/2009-INF issued by the Ministry of Finance dated 30th March, 2017 which incorporates a new sub sector "Affordable housing" under the category of "Social and Commercial Infrastructure"

Now, lets understand the conditions imposed under sec 80-IBA to claim a deductions in respect of profits and gains from housing projects

Majorly, the conditions of 80-IBA can be divided into six categories, detailed as below

A. PROJECT

- should be only housing project on the plot of land

- project approved after 1st June, 16 but on or before 31st Mar, 2019

- to be completed within 5 years from the date of approval

B. PLOT AREA

- land measuring not less than 1000 sqm in Mumbai, Kolkata, Delhi Chennai

- land measuring not less than 2000 sqm in any other place

C. FAR UTILISATION

- not less than 90% in Mumbai, Kolkata, Delhi Chennai

- not less than 80% in any other place

D. CARPET AREA

- Residential Unit

- should not exceed 30 sqm in Mumbai, Kolkata, Delhi Chennai

- should not exceed 60 sqm in any other place

- Shops and Other Commercial Establishments

- should not exceed 3 % of the aggregate carpet area of the project

E. ALLOTMENT

- Allotted to an Individual

- No other unit shall be allotted to the Individual or the spouse or the minor children of such individual

F. BOOKS OF ACCOUNT

- assessee should maintain separate books of account in respect of the housing project

Notification of Ministry of Finance vide notification no. 13/6/2009-INF dated 30th March, 2017 brought affordable housing within the ambit of Infrastructure sector and defines affordable housing as below -

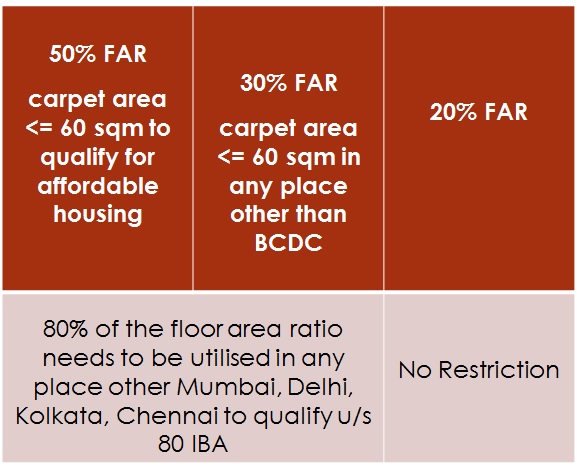

"Affordable housing is defined as a housing project using at least 50% of the Floor Area Ratio (FAR) / Floor Space Index (FSI) for dwelling units with carpet area of not more than 60 square meters"

Thus, a net inference from the conjoint reading of both the clauses i.e., to develop an affordable housing and claim the benefit of profit deduction u/s 80-IBA, will be something like this -

MASTER STROKE by the central government of India in defining affordable housing with FAR utilisation of 50% with a restriction of 60 sqm carpet area AND giving benefit u/s 80-IBA with a FAR utilisation of 90% / 80% and a restriction of 30 / 60 sqm of carpet area within the cities of Mumbai (B), Kolkata (C), Delhi (D), Chennai (C) and any other places respectively.

I hope this article will help in understanding the joint inference of the provisions of sec 80-IBA and affordable housing.

Please give your valuable feedback in the comments below.